In school we all learned the Theory of Supply and Demand. When the demand for an item is greater than the supply of that item, the price will surely rise.

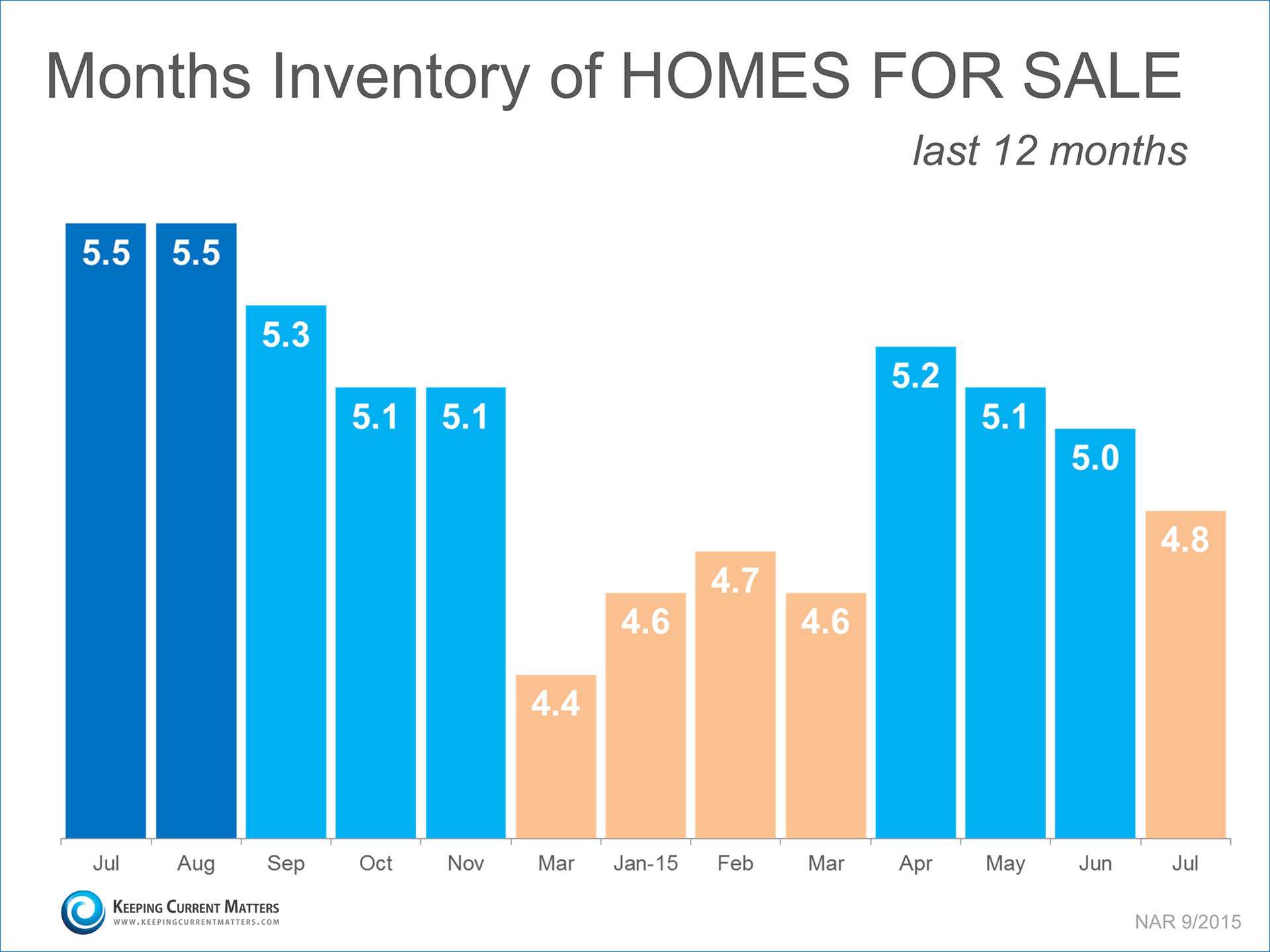

SUPPLY

The National Association of Realtors (NAR) recently reported that the inventory of homes for sale stands at a 4.8-month supply. This is significantly lower than the 6 months inventory necessary for a normal market.

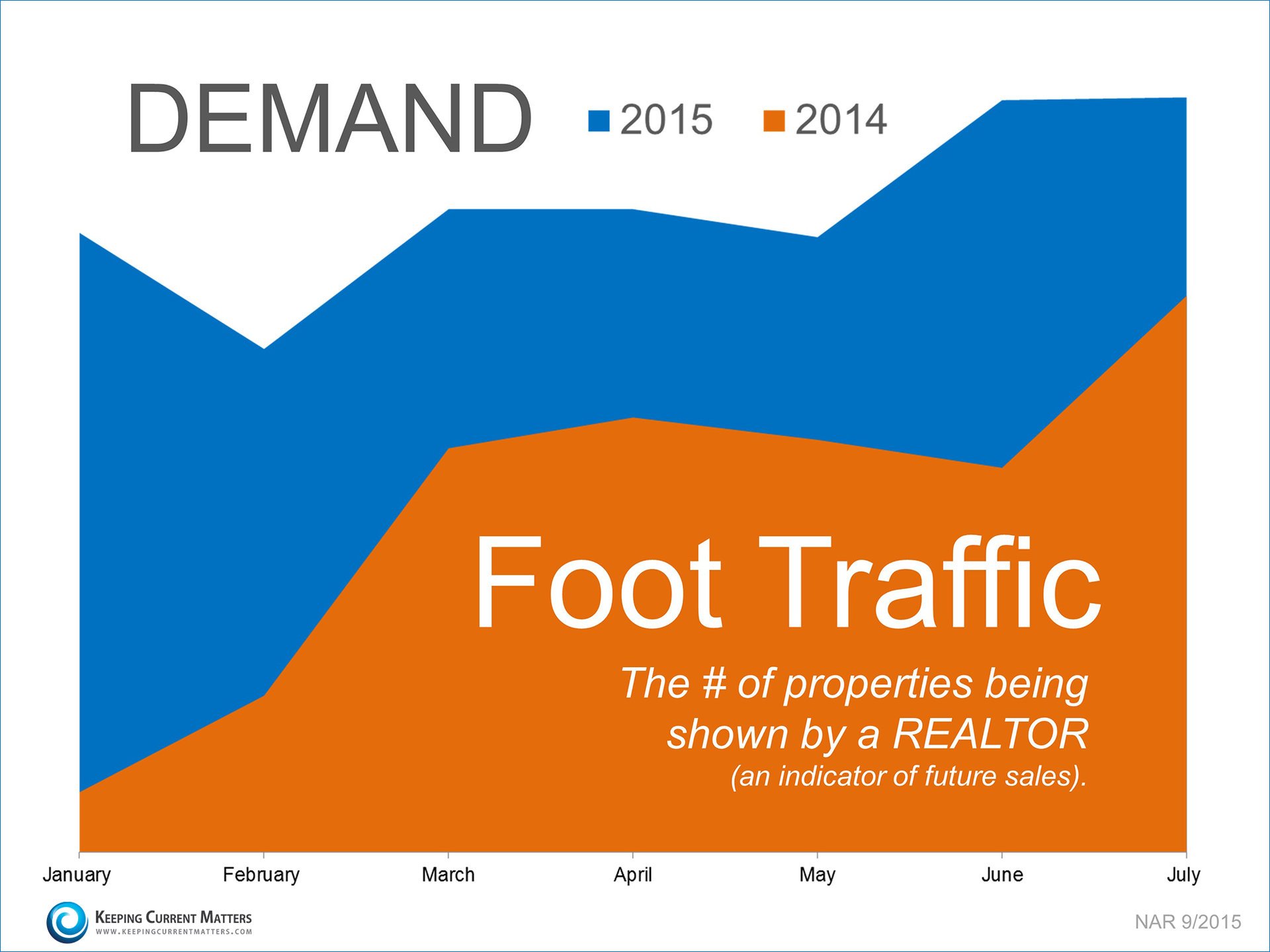

DEMAND

Every month NAR reports on the amount of buyers that are actually out in the market looking for homes, or foot traffic. As seen in the graph below, buyer demand this year has significantly surpassed the levels reached in 2014.

Many buyers are being confronted with a very competitive market in which they must compete with other buyers for their dream home (if they even are able to find a home they wish to purchase).

Listing your house for sale now will allow you to capitalize on the shortage of homes for sale in the market, which will translate into a better pricing situation.

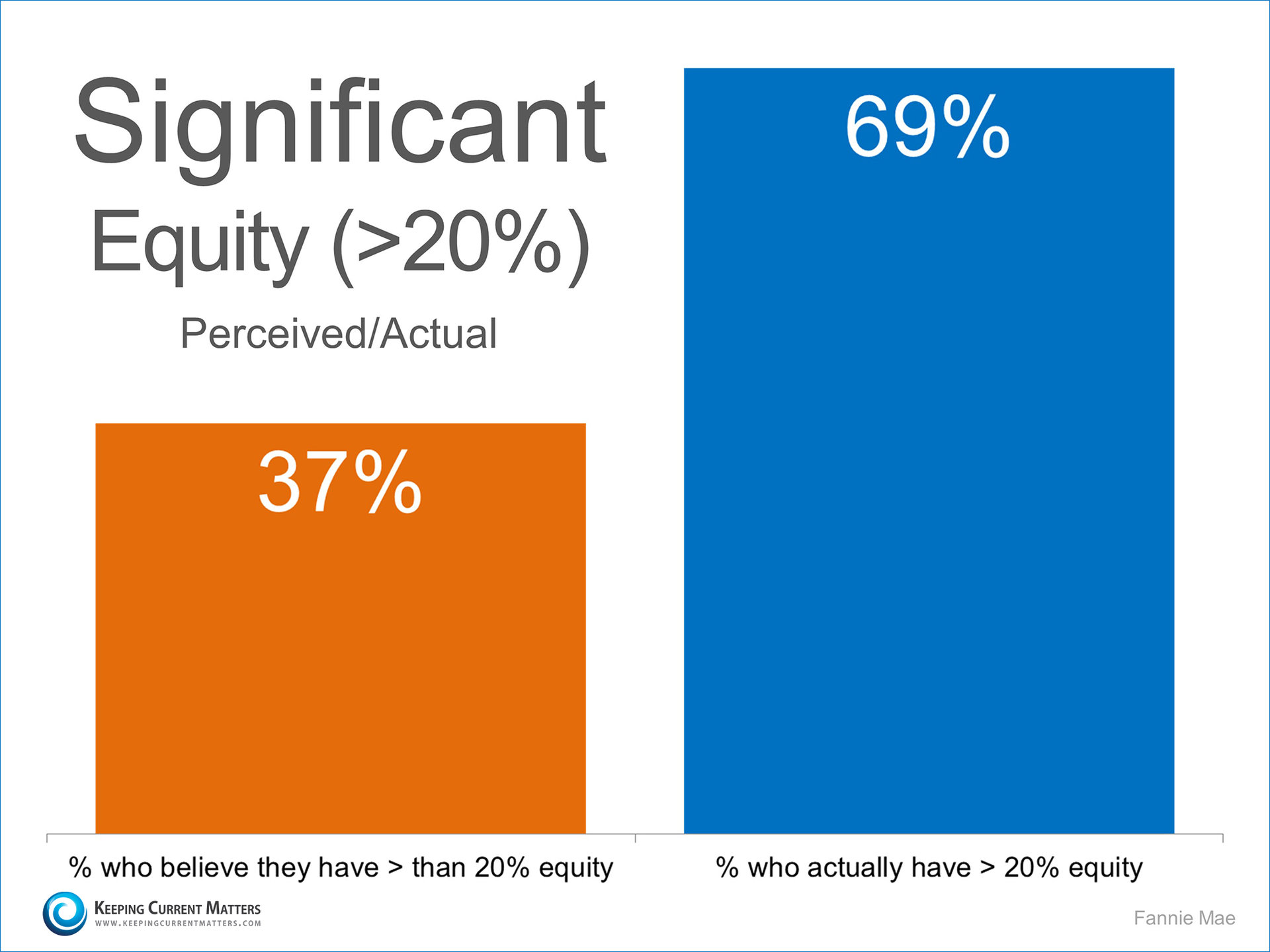

HOME EQUITY

Many homeowners underestimate the amount of equity they currently have in their home. According to a recent Fannie Mae study, 37% of homeowners believe that they have more than 20% equity in their home. In reality 69% of homeowners actually do!

Many homeowners who are undervaluing their home equity may feel trapped in their current home, which may be contributing to the lack of inventory in the market.

Bottom Line

If you are debating selling your home this year, meet with a local real estate professional that can evaluate the equity you have in your home and the opportunities available in your market.

![Economic Impact of Every Home Sold [INFOGRAPHIC] | Keeping Current Matters](http://www.keepingcurrentmatters.com/wp-content/uploads/2015/09/Economic-Impact.jpg)

![A+ Reasons To Hire A Real Estate Professional [INFOGRAPHIC] | Keeping Current Matters](http://www.keepingcurrentmatters.com/wp-content/uploads/2015/08/A-Reasons-To-Use-A-RE-Pro.jpg)